Virginia’s rolling hills, coastal plains, and mountain views offer diverse settings for tiny house living. Whether someone’s downsizing, seeking a minimalist lifestyle, or looking for an affordable housing alternative, the Commonwealth has become an increasingly popular spot for compact homes. Finding the right tiny house for sale in Virginia requires understanding local markets, zoning restrictions, and financing realities. This guide walks through where to look, what regulations apply, and how to secure a tiny home that fits both lifestyle and budget.

Key Takeaways

- Virginia’s diverse geography, moderate climate, and growing tiny house-friendly communities make it an attractive state for compact home living and downsizing.

- Tiny houses for sale in Virginia can be found through online marketplaces, local builders, and RV dealerships, with custom builds ranging from $50,000 to $100,000+ depending on size and finishes.

- Zoning laws vary significantly across Virginia counties—confirm local regulations, building codes (IRC Appendix Q), and permitted utility systems with your county’s building department before purchasing.

- Financing options for tiny homes include personal loans, RV loans for RVIA-certified homes, chattel loans, and land-home mortgage packages, with interest rates typically ranging from 4% to 12%.

- Budget for additional costs including property taxes ($200–$800 annually), homeowners or RV insurance ($400–$1,500 yearly), and septic/utility permits to avoid unexpected expenses when buying a tiny house in Virginia.

Why Virginia Is a Great State for Tiny House Living

Virginia’s geographic diversity makes it attractive for tiny house enthusiasts. From the Blue Ridge Mountains to the Chesapeake Bay coastline, buyers can choose settings that range from rural farmland to suburban communities.

The state’s moderate climate means less extreme heating and cooling demands compared to northern or southern regions. A well-insulated tiny house with a mini-split HVAC system (typically 12,000 BTU for spaces under 400 square feet) handles Virginia’s seasons without overworking the system.

Virginia also has a growing network of tiny house-friendly communities and RV parks that welcome RVIA-certified tiny homes on wheels. Some counties have updated ordinances to allow accessory dwelling units (ADUs) on existing residential lots, opening doors for foundation-built tiny homes as secondary structures.

Cost of living varies widely across the state. Rural counties like Floyd and Grayson offer lower land prices, often $3,000 to $8,000 per acre, making it feasible to buy land and place a tiny house. Urban areas near Richmond or Northern Virginia command higher prices but provide closer access to employment and amenities.

The state’s relatively relaxed stance on alternative housing compared to neighboring states has attracted builders, suppliers, and a community of tiny house advocates. That infrastructure makes sourcing materials, finding skilled trades, and connecting with other owners easier than in markets where tiny homes remain niche.

Where to Find Tiny Houses for Sale in Virginia

Online Marketplaces and Specialty Retailers

Several online platforms aggregate tiny house listings nationwide, including Virginia-specific inventory. Websites like Tiny House Listings, Tiny House Marketplace, and even Facebook Marketplace feature both new and used models. Filters by state, price range, and whether the home is on wheels or a foundation help narrow searches.

Many homes listed online come from out-of-state sellers, so verifying delivery logistics and associated costs is essential. Transporting a tiny house from across the country can add $3 to $5 per mile, which adds up fast.

RV and mobile home dealerships sometimes carry RVIA-certified tiny homes. These units meet National Fire Protection Association (NFPA) 1192 standards for recreational vehicles, which can simplify permitting in some Virginia jurisdictions that treat them as RVs rather than permanent dwellings.

Architecture and design platforms like Apartment Therapy occasionally feature tiny house tours and sale announcements, offering inspiration alongside practical listings. Real estate sites such as Zillow and Realtor.com have begun adding tiny house categories, though availability in Virginia fluctuates.

Buyers should confirm whether a listed home includes appliances, furniture, and utilities hookups. Some sellers offer turnkey models with propane or electric ranges, composting toilets, and 30-amp or 50-amp electrical service, while others sell shells requiring finish work.

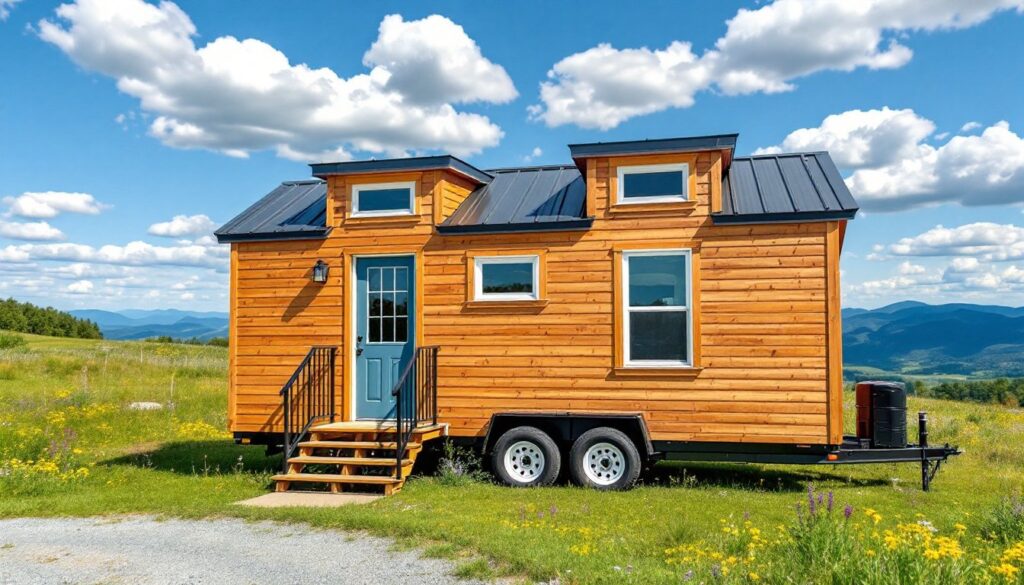

Local Builders and Custom Tiny Home Manufacturers

Working with a Virginia-based builder allows for customization and local code compliance. Several manufacturers operate in or serve the state, offering designs that range from rustic cabins to modern minimalist boxes.

Custom builds typically start around $50,000 for basic models (under 200 square feet) and can exceed $100,000 for larger homes (300-400 square feet) with high-end finishes. Builders familiar with Virginia’s International Residential Code (IRC) Appendix Q, which provides guidelines for tiny houses, can design to meet structural, egress, and loft ladder requirements.

Local builders also understand regional material availability. Virginia lumber yards stock standard dimensional lumber like 2x4s (actual dimensions 1.5″ x 3.5″) and 2x6s (1.5″ x 5.5″), which are common in tiny house framing. Sourcing locally cuts transportation costs and supports regional suppliers.

Many builders offer factory tours, allowing buyers to see construction quality firsthand. Checking for proper flashing around windows, adequate insulation (R-13 minimum in walls, R-30 in roofs for Virginia’s climate zone), and quality fasteners in trailer-to-frame connections is easier in person.

Buyers should request references and photos of completed projects. Reviewing past work helps assess craftsmanship and whether the builder’s style aligns with the buyer’s vision. Deposits typically range from 10% to 30% upfront, with progress payments tied to construction milestones.

What to Know Before Buying a Tiny House in Virginia

Zoning Laws and Building Codes Across Virginia Counties

Virginia grants counties and municipalities significant control over zoning and building regulations, so rules vary widely. Some areas welcome tiny houses: others restrict them entirely.

Permanent foundation tiny houses often fall under the IRC, which Virginia adopted with state-specific amendments. Appendix Q of the IRC addresses homes between 120 and 400 square feet, covering ceiling heights (6’8″ minimum in most areas, 6’4″ in lofts and bathrooms), egress window sizes (5.7 square feet minimum opening), and loft ladder specifications.

Counties like Albemarle and Loudoun have adopted ADU ordinances allowing tiny houses as secondary dwellings on lots with existing primary residences. These typically require the ADU to match the architectural style of the main house, stay under a certain square footage (often 800-1,000 square feet max), and meet setback requirements (usually 5-10 feet from property lines).

Tiny houses on wheels (THOWs) face trickier regulations. If certified by the Recreational Vehicle Industry Association (RVIA), they’re classified as RVs and may be allowed in RV parks or on private land zoned for recreational vehicles. But, many counties prohibit using RVs as permanent residences.

Some jurisdictions classify non-RVIA THOWs as movable structures, falling into a regulatory gray area. Without clear classification, obtaining permits and utility hookups becomes difficult. Prospective buyers should contact the local building department and zoning office before purchasing land or a tiny house.

Certain rural counties have minimal zoning enforcement, but that doesn’t mean regulations don’t exist. Building without permits can lead to fines, forced removal, or difficulties selling the property later. When considering pet-friendly spaces or specialized layouts, compliance with local codes remains essential.

Utility connections also vary by county. Municipal water and sewer hookups require permits and inspections. Off-grid systems, like composting toilets, rainwater collection, and solar panels, may need separate approvals. Virginia allows rainwater harvesting, but potable water systems must meet Virginia Department of Health standards.

Septic systems for tiny houses under 400 square feet still require county health department permits. A conventional septic system costs $3,000 to $7,000 installed, though some counties allow alternative systems like sand mounds or aerobic treatment units depending on soil conditions.

Electrical work must comply with the National Electrical Code (NEC). Most tiny houses use either a 30-amp service (common in RVs) or 50-amp service for homes with electric ranges and multiple appliances. A licensed electrician should handle the service panel installation and utility connection. Buyers tackling DIY electrical should pull permits and schedule inspections, unpermitted work can void insurance and complicate resales.

For buyers interested in accessible designs, Virginia’s Fair Housing Act and ADA guidelines don’t mandate residential accessibility, but planning for wider doorways (36″ clear opening minimum) and no-step entries adds long-term value.

Financing Options for Your Virginia Tiny Home Purchase

Financing a tiny house differs from a traditional mortgage. Most lenders won’t write conventional loans for homes under 400 square feet or those not permanently affixed to land.

Personal loans are a common route. These unsecured loans range from $10,000 to $100,000 with terms of 3 to 7 years. Interest rates typically run higher than mortgages, 6% to 12% depending on credit score, but approval is faster and doesn’t require the home to meet specific construction standards.

RV loans apply to RVIA-certified tiny houses on wheels. These secured loans use the tiny house as collateral, offering terms up to 15 years and rates between 4% and 8%. The home must have a VIN (vehicle identification number) and meet RVIA standards. Lenders like LightStream and other RV financing companies serve this market.

Chattel loans work for tiny houses on wheels or modular homes not attached to a foundation. These loans treat the home as personal property rather than real estate. Terms usually max out at 15 to 20 years with interest rates around 5% to 9%.

Land and home packages can qualify for traditional mortgages if the tiny house is permanently affixed to owned land. The combined value of land and home must meet the lender’s minimum loan amount, often $50,000 or more. The home must also meet local building codes and appraisal standards.

Some buyers finance through construction loans when working with a builder. These short-term loans (12 to 18 months) cover building costs, then convert to a traditional mortgage once construction is complete. The home must meet standard lending criteria, which can be challenging for sub-400-square-foot builds.

Credit unions sometimes offer more flexibility than national banks. Virginia-based credit unions familiar with alternative housing may structure loans specifically for tiny homes, especially for members with strong credit histories.

Cash purchases remain common in the tiny house market. Buyers saving $40,000 to $80,000 avoid interest and loan approval hurdles. Some finance through home equity loans or lines of credit on existing properties, leveraging lower interest rates.

Regardless of financing method, buyers should factor in insurance costs. Homeowners insurance for foundation-built tiny houses runs $400 to $1,000 annually depending on location and coverage. RVIA-certified THOWs typically require RV insurance, which costs $600 to $1,500 per year. Non-RVIA mobile tiny houses may need specialty insurance, which can be harder to source.

Property taxes apply to tiny houses on permanent foundations based on assessed value. Rural Virginia counties often assess tiny homes at $20,000 to $60,000, resulting in annual taxes of $200 to $800. THOWs classified as RVs may avoid property taxes but could face personal property taxes instead, depending on county rules.

Understanding parking regulations helps buyers plan where their home will sit, which directly impacts financing eligibility and insurance requirements. Platforms like Curbed track real estate trends that influence tiny house markets, while resources like ImproveNet offer cost guides for renovations and upgrades once the home is purchased.

Buyers should shop multiple lenders, compare APRs, and read loan terms carefully. Some lenders charge origination fees (1% to 5% of loan amount) or prepayment penalties. Getting pre-approved before shopping helps set a realistic budget and strengthens negotiating position with sellers or builders.